How to Buy a Bankruptcy House as an Investor

Bankruptcy house investing can create opportunities for real estate investors, but it is not the same as buying a standard foreclosure, REO property, or off-market distressed home. When a property is involved in bankruptcy, the sale may be controlled by a trustee, a debtor, a lender, the bankruptcy court, or some combination of those parties.

That means your offer may not be enough by itself. You may also need court approval, creditor notice, lien review, sale confirmation, and more patience than a typical distressed-property transaction requires.

If you approach the deal correctly, a bankruptcy house can become a profitable acquisition. If you misunderstand the process, you can tie up time, capital, and legal fees without ever reaching closing.

Stay Ahead of the Next Deal

Markets move quickly, and good foreclosure opportunities often require fast analysis. Subscribe to our twice-weekly newsletter for investor-focused tips, tools, and market insights designed to help you make better decisions.

What Is a Bankruptcy House?

A bankruptcy house is a property connected to a bankruptcy case. The owner may have filed Chapter 7, Chapter 11, or Chapter 13 bankruptcy. The property may be part of the bankruptcy estate, protected by the automatic stay, listed for sale by a trustee, or subject to a lender’s request to continue foreclosure.

In a Chapter 7 case, the trustee may liquidate non-exempt assets to pay creditors. The U.S. Courts’ explanation of Chapter 7 bankruptcy is relevant to investors because it explains that a trustee may sell property that is not protected by exemptions.

For you as an investor, the key question is simple: who has authority to sell the house?

If the debtor still controls the sale, the transaction may look more like a short sale or distressed listing, but with bankruptcy court involvement. If a trustee controls the sale, you may be negotiating with a fiduciary whose job is to maximize value for the estate and creditors.

Why Bankruptcy Changes the Buying Process

The Automatic Stay Can Pause Foreclosure

When someone files bankruptcy, the automatic stay generally stops collection activity, including many foreclosure actions. This can interrupt an auction, delay a lender’s timeline, or freeze a deal that seemed close to closing.

The U.S. Courts’ explanation of the automatic stay matters because it shows why a lender, investor, or buyer cannot always move forward just because a property is in default.

This is where timing risk enters the deal. A property can be distressed, vacant, underwater, or badly neglected, but still not available for immediate purchase if the bankruptcy court has not cleared the path.

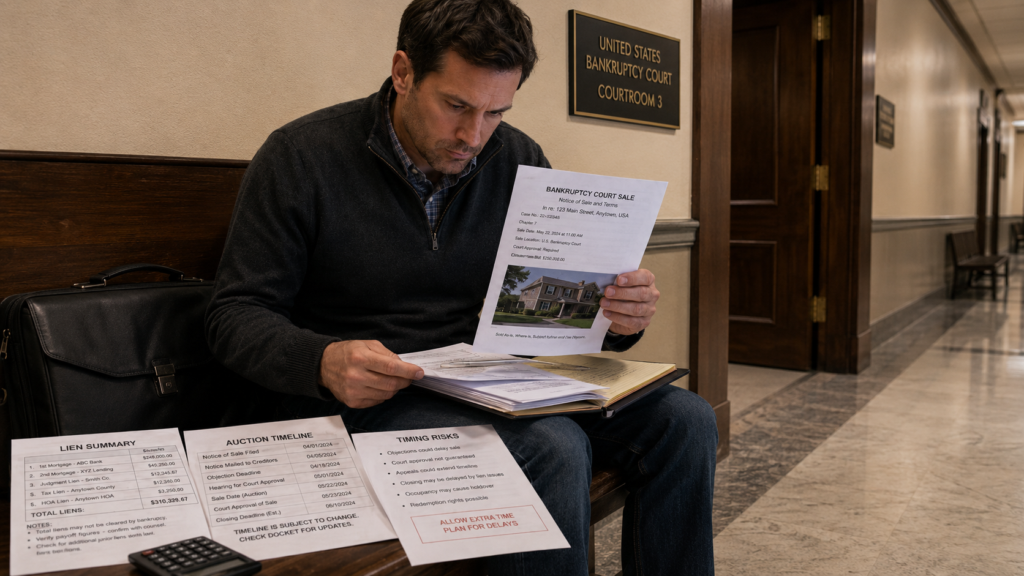

A Trustee Sale May Need Court Approval

If a bankruptcy trustee is selling the house, the trustee may accept an offer, but that does not always mean the deal is final. Bankruptcy sales often require notice to interested parties and approval from the bankruptcy court.

This creates a different type of acquisition risk. You might spend time negotiating, inspecting, arranging financing, and preparing closing documents, only to face an objection, competing offer, overbid opportunity, or court-related delay.

A bankruptcy sale is often not final until the court approves it. That court-approval issue is a core part of buying property in bankruptcy, and you should treat it as part of your closing risk from the beginning.

How to Find Bankruptcy House Opportunities

Public Records and Court Filings

Bankruptcy cases are filed in federal court, while property records are usually maintained locally. You may need to connect several pieces of information: the bankruptcy filing, the property address, the debtor’s ownership interest, the mortgage status, and any sale motion or trustee activity.

This is not always beginner-friendly research. The property may not be advertised as a “bankruptcy house.” It may appear as a foreclosure delay, an estate sale, a trustee sale, a distressed MLS listing, or a court-approved sale.

Attorneys, Trustees, and Distressed Property Networks

Some opportunities come through bankruptcy attorneys, real estate agents who handle court-approved sales, trustees, auction platforms, or investor networks. The process can be less public than a foreclosure auction but still more formal than a direct seller negotiation.

You should be ready to show proof of funds, clear contract terms, and realistic closing ability. A trustee or court may not want a buyer who needs too many contingencies or an uncertain financing path.

Due Diligence Before You Make an Offer

Confirm Sale Authority

Before you underwrite the deal too deeply, confirm who can actually sell the property. Is the debtor selling it? Is the trustee selling it? Is the lender foreclosing after receiving stay relief? Is the court required to approve the sale?

This matters because the wrong signature on a contract may not give you a valid path to closing. You need the seller’s legal authority to match the bankruptcy status.

Review Liens and Payoffs

Bankruptcy does not automatically erase every lien attached to the property. Mortgage liens, tax liens, municipal liens, HOA claims, judgment liens, and other encumbrances may still need to be addressed through the sale process.

You should work from a title commitment, payoff information, court filings, and local lien searches. Do not rely only on the seller’s verbal description of the debt.

The U.S. Trustee Program’s guidance on Chapter 7 trustee administration reinforces that trustees are fiduciaries managing estate assets. For investors, that means the trustee’s job is not to give you a bargain. The trustee’s job is to administer the asset for the estate.

Understand Occupancy and Possession

A bankruptcy house may be occupied by the debtor, a tenant, a family member, or an unknown occupant. Bankruptcy can complicate possession because timing may depend on court orders, lease rights, foreclosure status, or negotiated move-out terms.

If you are planning to flip the property, delayed possession can push back inspections, utility activation, contractor scheduling, permits, and resale. If you are planning to rent the property, you need to know whether an existing tenant has rights that survive the sale.

How to Underwrite a Bankruptcy House

Start With the Same Core Numbers

Your basic deal math still starts with ARV, repairs, holding costs, financing costs, selling costs, and required profit. The bankruptcy layer does not replace normal underwriting. It adds risk adjustments.

Your maximum offer should reflect:

- Court approval delay.

- Possible overbid risk.

- Legal review costs.

- Title curative work.

- Occupancy uncertainty.

- Lien payoff uncertainty.

- Longer closing timeline.

- Higher holding-cost assumptions.

If the deal only works with a perfect timeline, it is probably too thin.

Add a Bankruptcy Timing Reserve

You should include a timing reserve in the budget. Even a strong deal can become weaker if it takes 60 to 120 additional days to receive court approval, clear objections, resolve title issues, or obtain possession.

Hard money lenders may also view the deal differently if closing depends on court approval. Before you commit earnest money, confirm that your lender understands the sale structure and can fund within the expected timeline.

Learn the Strategies Behind Smarter Foreclosure Investing

Get practical foreclosure investing content delivered twice a week, including deal analysis tips, strategy breakdowns, useful tools, and new resources from Foreclosure Flips. Sign up to keep learning and spotting better opportunities.

Offer Strategy for Bankruptcy House Investing

Keep the Contract Clean

A trustee or court may prefer a clean offer over a complicated one. That does not mean you should waive essential due diligence blindly. It means your offer should be clear, fundable, and realistic.

If you include contingencies, make them specific. Avoid vague language that creates confusion. Make sure the contract explains deposit requirements, inspection access, title review, court approval, closing deadline, and what happens if approval is delayed or denied.

Be Prepared for Overbids

In some bankruptcy sales, your accepted offer can become the stalking horse or baseline bid. Other buyers may have an opportunity to submit higher offers before or during the approval process.

That can be frustrating, but it is part of the system. The estate may be trying to maximize value for creditors. You need to decide in advance whether you will increase your offer or walk away.

The Investor Takeaway

Bankruptcy house investing can be profitable, but you need to respect the process. A bankruptcy property is not just a distressed house. It may be an asset of a bankruptcy estate, subject to court approval, creditor notice, lien review, sale procedures, and timing risk.

Your best protection is disciplined underwriting. Confirm who has authority to sell, understand whether court approval is required, review liens carefully, budget for delays, and avoid assuming that an accepted offer is final before the court signs off.

A bankruptcy house can be a strong investor opportunity when the discount is large enough to justify the added complexity.

But the profit is not created by the word “bankruptcy.” It is created by buying with clear authority, clean numbers, and enough margin to survive the process.

Looking for Deeply Discounted Properties Others Don’t Know About?

Don’t miss out on the next great investment opportunity! Search millions of foreclosure listings and get daily alerts for new properties in your target market.

You might also like:

Tax Delinquency vs Mortgage Foreclosure for Investors

Tax Delinquency vs Mortgage Foreclosure for Investors

Housing Affordability Crisis and Foreclosure Investing

Housing Affordability Crisis and Foreclosure Investing

Occupied Foreclosure Properties: What Investors Need to Know

Occupied Foreclosure Properties: What Investors Need to Know

How HOA Liens Can Change a Foreclosure Deal

How HOA Liens Can Change a Foreclosure Deal

The Investor Foreclosure Funnel Explained in 6 Steps

The Investor Foreclosure Funnel Explained in 6 Steps

Auction Houses vs Online Foreclosure Auctions

Auction Houses vs Online Foreclosure Auctions