How to Build an Accurate ARV Analysis [Free Worksheet]

Accurate ARV analysis is one of the most important skills in real estate investing.

The after-repair value affects the offer, the renovation budget, the financing plan, the projected profit, and the decision to buy or pass. It matters for flips, BRRRR projects, new construction, rental repositioning, and small development.

A weak ARV estimate can make a bad deal look good. A disciplined ARV estimate can keep an investor out of trouble.

The challenge is that many investors still treat ARV too casually. They pull a few nearby sales, average the numbers, and assume the deal works. That may be fast, but it is not analysis.

Get the Free ARV Analysis Worksheet

Before making an offer, make sure the numbers support the deal. Subscribe to the Foreclosure Flips 2X weekly newsletter and get our free ARV Analysis Worksheet to help you compare comps, estimate after-repair value, and evaluate potential profit before moving forward.

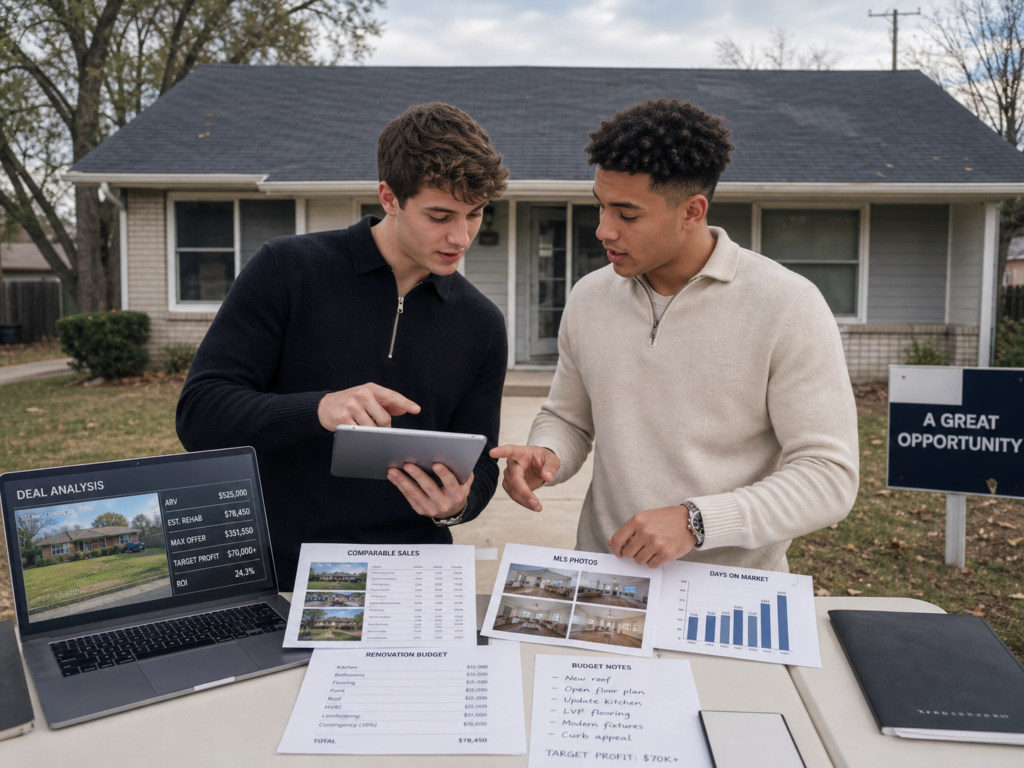

ARV Is a Market-Supported Opinion

ARV is not what the investor wants the property to be worth. It is not what the seller says it could be worth. It is not the highest nearby sale. It is a supported estimate of what the property may sell for after the planned improvements are complete.

That means the investor needs relevant comparable sales.

Fannie Mae states that the sales comparison approach uses comparable sales to support an opinion of market value and requires at least three closed comparable sales in appraisal reporting. Current listings and contract offerings can also be used as supporting data when appropriate. Fannie Mae’s comparable sales guidance is directly relevant to how investors should think about comp discipline.

Investors do not need to produce a formal appraisal. But they do need to build a value opinion that can survive scrutiny.

Relevance Beats Quantity

More comps do not automatically mean a better ARV.

Ten weak comps are less useful than three strong comps.

A relevant comp should generally be similar in location, size, property type, age, condition, layout, lot utility, bedroom and bathroom count, and buyer appeal. It should also be recent enough to reflect current market conditions.

HUD’s valuation guidance notes that sales data should generally not exceed six months between the comparable sale date and the appraisal date, and sales beyond six months require explanation; it also states that comparable sales must not exceed twelve months in that guidance context. HUD Handbook 4150.2 valuation guidance is useful for understanding why older sales become less reliable without market support.

For investors, the lesson is clear. A sale from two years ago may be interesting, but it may not support today’s ARV unless the market has been carefully adjusted.

Condition Is Often the Missing Variable

The most common ARV mistake is comparing properties without understanding condition.

A house that sold for $500,000 may appear to support the investor’s ARV. But if that comp had luxury finishes, an open layout, new mechanical systems, a finished basement, professional staging, and a superior lot, it may not support a basic cosmetic rehab.

Condition must be verified whenever possible.

Photos, agent remarks, listing history, and renovation descriptions can help the investor determine whether a comparable sale really matches the subject property’s planned finished condition.

This matters because buyers pay for product. They are not only buying square footage. They are buying layout, design, condition, finishes, utility, and confidence.

Compare the Planned Product to the Sold Product

A good ARV analysis asks: what will the finished property compete against?

If the investor plans to renovate a property to rental-grade finishes, it should not be valued against high-end retail flips. If the investor plans to build a new duplex, it should not be valued using dated single-family sales unless the analysis clearly adjusts for the differences.

The planned product should match the comps being used.

That includes interior finishes, exterior appeal, functionality, bedroom count, bathroom count, parking, outdoor space, and overall buyer or renter expectations.

In a competitive market, the difference between average and exceptional finishes can be meaningful. In a slower market, over-improving may not produce a sufficient return.

Days on Market Helps Test Demand

Days on market can provide important context.

A property that sold quickly at or above list price may indicate strong demand. A property that sat for months and required price cuts may indicate weaker demand, overpricing, or product mismatch.

This does not mean a slow sale should always be ignored. Sometimes the property was overpriced at first. Sometimes the listing photos were poor. Sometimes the seller refused early offers. But days on market should be part of the analysis.

Investors should be careful when using comps that technically sold at a high number but only after a long marketing period. If the investor’s financing plan depends on a fast sale, a slow-moving comp may not support the strategy.

Adjust for Market Timing

Markets move.

Interest rates, inventory, buyer demand, local employment, seasonality, and competing listings can all affect resale value. A sale from six months ago may not mean the same thing in a rising market as it does in a declining market.

Fannie Mae’s 2025 market condition adjustment guidance states that property value trends may be categorized as increasing, stable, or declining, and that market condition adjustments are based on changes between the comparable sale’s contract date and the effective date of the appraisal. Fannie Mae’s market condition adjustment guidance is useful for investors because it emphasizes that timing matters when interpreting comps.

An investor does not need to make appraisal-style adjustments in every analysis. But ignoring market direction is dangerous.

Get the Free ARV Analysis Worksheet

Before making an offer, make sure the numbers support the deal. Subscribe to the Foreclosure Flips 2X weekly newsletter and get our free ARV Analysis Worksheet to help you compare comps, estimate after-repair value, and evaluate potential profit before moving forward.

Active and Pending Listings Add Forward-Looking Context

Closed sales show what buyers paid in the recent past. Active and pending listings help show what the subject property may compete against when it is finished.

Active listings are not completed sales, so they should not be treated the same as sold comps. Sellers can ask any price they want. But active listings can reveal current competition, pricing pressure, inventory levels, and product quality.

Pending listings can be even more useful because they show properties that have attracted buyers, although the final sale price may not be known until closing.

Fannie Mae’s Market Conditions Addendum states that sales and listings used in market analysis must be properties that compete with the subject property, using criteria a prospective buyer would apply. It also requires explanation of anomalies such as seasonal markets, new construction, and foreclosures. Fannie Mae’s market conditions addendum reinforces the importance of competitive market context.

For investors, this means ARV analysis should not stop at closed sales. It should also consider what else buyers will see when the finished property hits the market.

Avoid the Highest-Comp Trap

The highest nearby sale is not automatically the ARV.

Many investors make this mistake because the highest comp makes the deal look better. But if that sale is not truly comparable, it can create a false profit.

The best ARV estimate is usually built from a range of relevant comps, not a single optimistic data point.

The investor should identify the strongest comps, reject weak ones, understand the differences, and choose a value that reflects the likely market response to the finished property.

The Appraisal Institute’s sales comparison training emphasizes data collection, selection, verification, qualitative and quantitative analysis, and reconciliation. That final word matters. Reconciliation means weighing the evidence instead of blindly averaging prices. The Appraisal Institute’s residential sales comparison course provides helpful context on how comparison data is analyzed.

Put the ARV Inside the Full Deal Model

ARV should not be analyzed in isolation.

The investor should connect ARV to purchase price, renovation budget, financing costs, holding costs, selling costs, contingency, and required profit margin.

A strong ARV does not save a deal if the rehab budget is too low. A good purchase price does not save a deal if the finished value is overstated. A beautiful renovation does not save a deal if the market will not support the resale price.

A tool such as Rehab Valuator can help investors connect valuation assumptions to the larger project model, including budget, funding, and projected returns.

The more organized the analysis, the easier it is to see whether the deal actually works.

Mentorship Can Improve Judgment

Accurate ARV analysis is partly data and partly judgment.

Data shows the comps. Judgment determines which comps matter, which ones should be rejected, and how much weight each sale deserves.

That judgment improves through repetition, feedback, and exposure to real deals. Investors who only analyze in isolation can repeat the same mistakes for years.

For investors who want help developing better deal judgment, the Rehab Valuator Inner Circle Mentorship may be useful because ARV analysis is easier to improve when deals are reviewed in a community of experienced operators.

Test the Process on Real Deals

One way to improve ARV accuracy is to review completed projects after sale.

What ARV was projected? What did the property actually sell for? Which comps were used? Which comps turned out to be most relevant? Were active listings a warning sign? Did the property sit longer than expected? Did buyers respond to the finish level?

This feedback loop is essential.

For investors who want to test a more structured workflow for analyzing and reviewing deals, the 14-Day $1 Trial of Rehab Valuator Premium can be a practical way to organize the process.

The Bottom Line

Accurate ARV analysis is not about finding the highest sale and hoping the market agrees.

It is about selecting relevant comps, studying condition, reviewing photos, understanding days on market, checking sale history, adjusting for market timing, and considering active and pending competition.

The investor who gets ARV wrong may overpay before the project ever begins. The investor who gets ARV right has a much better chance of making disciplined offers, building realistic budgets, and protecting profit.

Better ARV analysis does not eliminate risk. It reduces guesswork.

Test Your Foreclosure Investing Knowledge

You’ve covered the basics. Now see how much you really understand about pre-foreclosures, auctions, short sales, flipping, BRRRR, ARV, repair budgets, title issues, and deal risk. Take the 15-question Foreclosure Investing Quiz and see how you score before you analyze your next deal.

Want to Reach More Real Estate Investors?

Put your brand in front of foreclosure investors, flippers, BRRRR buyers, and deal-focused readers. Advertise With Us

You might also like:

Renovation Budget for Flipping Houses That Won’t Break the Bank

Renovation Budget for Flipping Houses That Won’t Break the Bank

Project Management Software for House Flipping

Project Management Software for House Flipping

Finding Contractors for House Flips: The Investor’s Playbook

Finding Contractors for House Flips: The Investor’s Playbook

Estimating Renovation Costs for Flips: A Practical Guide + Free Worksheet

Estimating Renovation Costs for Flips: A Practical Guide + Free Worksheet

House Flipping: How to Find, Analyze, Renovate, and Sell a Profitable Flip

House Flipping: How to Find, Analyze, Renovate, and Sell a Profitable Flip

How Higher Interest Rates Affect Foreclosure Deals

How Higher Interest Rates Affect Foreclosure Deals