Investing in Chapter 7 vs Chapter 13 Real Estate Bankruptcy

Understanding Chapter 7 vs Chapter 13 real estate issues can help you avoid misreading a foreclosure opportunity. When a property owner files bankruptcy, the foreclosure timeline may pause, the sale may be delayed, and the property may not be available as quickly as you expected.

For investors, the bankruptcy chapter matters because it can affect who controls the property, whether the owner is trying to keep it, whether a trustee may sell it, and when a lender can continue foreclosure. You don’t need to become a bankruptcy attorney, but you do need to understand enough to avoid treating every bankruptcy property the same way.

Learn the Strategies Behind Smarter Foreclosure Investing

Get practical foreclosure investing content delivered twice a week, including deal analysis tips, strategy breakdowns, useful tools, and new resources from Foreclosure Flips. Sign up to keep learning and spotting better opportunities.

Why Bankruptcy Type Matters in Real Estate Investing

Bankruptcy can change the path of a distressed-property deal because it may trigger the automatic stay. That stay can pause foreclosure activity, collection efforts, and certain actions against the property while the bankruptcy case is pending.

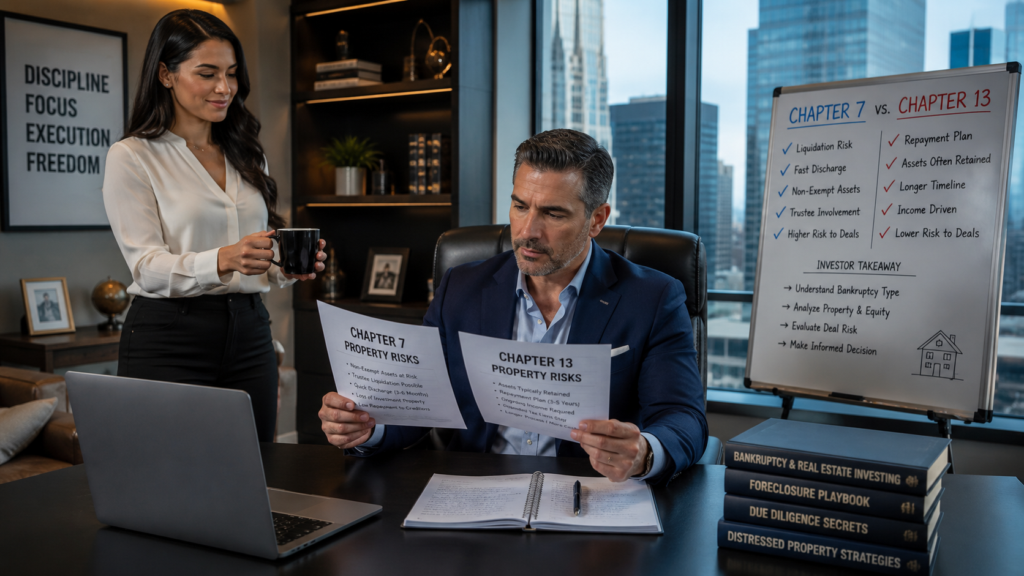

But Chapter 7 and Chapter 13 are not built around the same goal. Chapter 7 is generally a liquidation process. Chapter 13 is generally a repayment plan for individuals with regular income.

The National Consumer Law Center’s Chapter 7 and Chapter 13 comparison helps frame the practical difference: Chapter 7 may involve liquidation, while Chapter 13 is usually used to keep property while catching up over time.

That difference changes what you should expect as an investor.

What Chapter 7 Can Mean for a Property

Chapter 7 is often called liquidation bankruptcy. In a Chapter 7 case, a trustee may review the debtor’s assets and determine whether any non-exempt property can be sold to pay creditors.

For real estate investors, the key issue is equity. If the property has little or no non-exempt equity after liens, exemptions, sale costs, and trustee expenses, the trustee may not have a strong reason to sell it. If the property has meaningful non-exempt equity, a trustee sale may become possible.

The Property May Be Sold by a Trustee

A Chapter 7 property may become interesting if the trustee has authority and financial reason to sell. But this does not mean you can simply negotiate a normal purchase contract with the owner.

You need to know whether the property is part of the bankruptcy estate, whether the trustee is administering it, whether court approval is required, and whether the sale will be subject to creditor notice or overbid procedures. If the trustee is selling, the trustee’s job is usually to maximize value for the estate, not to give you a below-market deal.

The Lender May Still Foreclose Later

Chapter 7 does not automatically solve the borrower’s mortgage default. If the owner is behind on payments and does not reaffirm, redeem, sell, or otherwise resolve the secured debt, the lender may eventually seek permission to continue foreclosure.

This can create a tracking opportunity. A property may pause during bankruptcy, then later return to the foreclosure pipeline after the stay is lifted, the case is dismissed, or the lender completes the required process.

What Chapter 13 Can Mean for a Property

Chapter 13 usually works differently. The debtor proposes a repayment plan, typically over three to five years, and may use that plan to catch up on mortgage arrears while keeping the property.

The U.S. Courts’ Chapter 13 bankruptcy basics explain that Chapter 13 can allow individuals to keep property and pay debts over time, including using the process to save a home from foreclosure if the plan succeeds.

For you, that means a Chapter 13 filing often signals that the owner is trying to retain the property rather than sell it immediately.

The Deal May Be Delayed, Not Available

If you were tracking an auction date and the owner files Chapter 13, the sale may be postponed. The owner may be attempting to cure missed payments through the plan. If the plan is confirmed and payments are maintained, the foreclosure may not move forward.

That does not make the lead useless, but it changes the expected timeline. You may need to monitor the bankruptcy case, foreclosure docket, and property condition over time instead of assuming an acquisition opportunity is imminent.

The Plan Can Fail

Chapter 13 cases do not always succeed. If the debtor misses plan payments, fails to stay current on the mortgage, or cannot maintain the proposed repayment structure, the case may be dismissed or the lender may seek relief from the stay.

That can move the property back toward foreclosure. For investors, the opportunity may reappear later, but your original numbers may no longer apply. During the delay, taxes, HOA dues, code violations, deferred maintenance, and property damage may continue to accumulate.

Relief From Stay Can Reopen the Foreclosure Path

Whether the case is Chapter 7 or Chapter 13, a lender may ask the bankruptcy court for relief from the automatic stay. If granted, the lender may be able to continue foreclosure activity even while the bankruptcy case remains open.

Federal bankruptcy procedure matters here. Rule 4001 addresses motions for relief from the automatic stay, and Cornell’s Legal Information Institute summary of relief from stay procedure notes that an order granting relief is generally stayed for 14 days unless the court orders otherwise.

For investors, the practical lesson is simple: don’t rely on rumor. Track the actual court filings and sale notices.

How Chapter 7 vs Chapter 13 Changes Your Strategy

If It Is Chapter 7

In Chapter 7, you should ask whether the property has enough equity for a trustee sale, whether the trustee has abandoned the property, whether the lender is seeking stay relief, and whether the foreclosure will resume.

A Chapter 7 case may create an acquisition opportunity through a trustee sale, a court-approved sale, or a later foreclosure auction. But you need to confirm sale authority before spending too much time on the deal.

If It Is Chapter 13

In Chapter 13, assume the owner may be trying to keep the property unless the filings show otherwise. You should track whether the plan treats the mortgage, whether payments are being made, whether the lender has objected, and whether any stay-relief motion has been filed.

A Chapter 13 property may not be a near-term deal. It may be a watchlist asset.

What You Should Check Before Pursuing the Deal

Before you spend money on title work, inspections, or legal review, confirm the basic facts:

- Which bankruptcy chapter was filed.

- Whether the property is listed in the schedules.

- Whether the debtor claims an exemption.

- Whether a trustee is administering the asset.

- Whether the lender filed for relief from stay.

- Whether the foreclosure sale was postponed.

- Whether the case was dismissed, discharged, or converted.

- Whether the owner, trustee, or court has authority to sell.

You should also update the deal math. A delayed bankruptcy property may have higher unpaid taxes, more repair issues, increased legal complexity, and a longer holding-cost timeline than you originally expected.

The Investor Takeaway

Chapter 7 vs Chapter 13 real estate matters because each chapter points to a different distressed-property path. Chapter 7 may involve trustee review, liquidation risk, abandonment, or eventual foreclosure. Chapter 13 usually focuses on repayment and property retention, which can delay or stop a foreclosure if the plan succeeds.

As an investor, your job is to identify the bankruptcy chapter, confirm who controls the property, track court activity, and adjust your timeline. A bankruptcy filing does not automatically kill a deal, but it can change when the deal becomes available, who can approve the sale, and how much risk you need to price into your offer.

Wondering Where the Savviest Investors Find Their Best Deals?

Access the largest database of foreclosure properties nationwide and discover below-market deals before other investors. Start your search today!

You might also like:

How Bankruptcy Can Delay an Investment Foreclosure Deal

How Bankruptcy Can Delay an Investment Foreclosure Deal

Foreclosure Auction Tips That Could Save You Thousands

Foreclosure Auction Tips That Could Save You Thousands

How Foreclosure Redemption Periods Affect Investor Profit

How Foreclosure Redemption Periods Affect Investor Profit

Judicial vs Non-Judicial Foreclosure for Investors

Judicial vs Non-Judicial Foreclosure for Investors

How HOA Liens Can Change a Foreclosure Deal

How HOA Liens Can Change a Foreclosure Deal

Auction Houses vs Online Foreclosure Auctions

Auction Houses vs Online Foreclosure Auctions