Judicial vs Non-Judicial Foreclosure for Investors

Understanding judicial vs non-judicial foreclosure is essential before bidding on distressed property. The difference is not just legal terminology.

It can affect how long the process takes, how much uncertainty remains after the sale, how you calculate holding costs, and how aggressively you should bid.

For investors, foreclosure procedure shapes the deal before the auction ever happens.

Build Your Investing Knowledge One Email at a Time

Foreclosure investing rewards preparation. Join our 2X week newsletter for straightforward guidance on pre-foreclosures, short sales, BRRRR, flipping, and other strategies investors use to evaluate distressed property opportunities.

What Is Judicial Foreclosure?

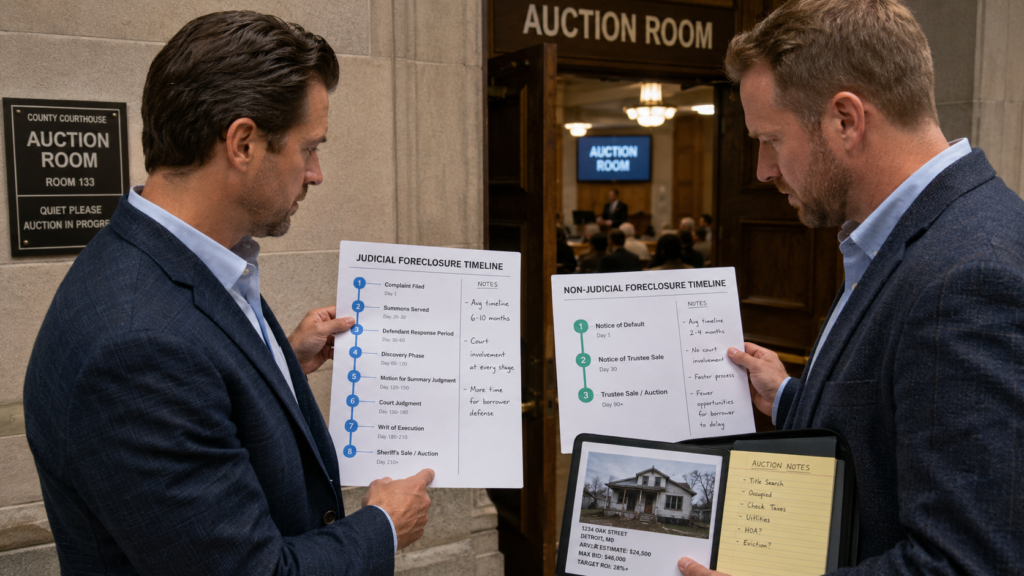

Judicial foreclosure means the lender must go through court to foreclose. The lender files a lawsuit, the borrower has an opportunity to respond, and the court must generally approve the foreclosure before the property can be sold.

That added court process can create a longer timeline. It may also introduce delays from borrower defenses, hearings, court backlogs, settlement discussions, or sale objections.

The Consumer Financial Protection Bureau’s summary of the foreclosure process confirms that foreclosure procedures differ by state and are generally handled either through court or outside court under state law.

Why Judicial Foreclosure Matters to Investors

Judicial foreclosure can give investors more time to research a property before the final sale, but it can also make timing less predictable.

If you are tracking a potential deal for months, you may see continued deterioration, added liens, occupancy complications, or changing market conditions before you ever get a chance to bid.

That means your numbers need a wider margin of safety. A judicial foreclosure deal may require more conservative assumptions around repair costs, resale timing, and carrying costs.

What Is Non-Judicial Foreclosure?

Non-judicial foreclosure allows the lender or trustee to foreclose without filing a court lawsuit, assuming state law and the loan documents allow it. These foreclosures are often tied to a deed of trust or a power-of-sale clause.

The National Association of Realtors notes that a nonjudicial mortgage foreclosure can take about 120 days in some contexts, while judicial foreclosure timelines vary significantly by state.

Its short sales and foreclosures guidance reinforces why investors should treat procedure and timeline as part of deal analysis, not as background detail.

Why Non-Judicial Foreclosure Matters to Investors

Non-judicial foreclosure can move faster, which may create opportunity for investors who are organized and ready to act. The downside is that the shorter timeline can reduce your research window.

You may have less time to verify title issues, inspect from the exterior, estimate repairs, confirm occupancy, line up financing, and understand local auction procedures. A faster sale process does not automatically mean a cleaner deal.

How Procedure Changes Your Bidding Strategy

Timeline Risk

In judicial foreclosure states, your main risk may be delay. In non-judicial foreclosure states, your main risk may be speed. Both can hurt returns.

A delayed judicial foreclosure can tie up your attention and financing plan. A fast non-judicial auction can pressure you into bidding before you fully understand the property.

Closing Certainty

Non-judicial sales may feel more straightforward, but investors still need to confirm notice requirements, trustee procedures, title status, redemption rights, and whether any legal challenge could affect the sale.

State-specific rules can vary substantially, as shown in Nolo’s judicial and nonjudicial foreclosure chart.

Financing and Exit Planning

If you are using hard money, every extra month matters. Judicial foreclosure delays can affect rate locks, lender approvals, and capital availability. Non-judicial foreclosure speed can create a different problem: you may need funds ready before your due diligence is complete.

Either way, your bid should reflect the process.

The Investor Takeaway

The difference between judicial vs non-judicial foreclosure can change the economics of a deal. Judicial foreclosure may give you more time but less timeline certainty. Non-judicial foreclosure may move faster but require stronger preparation before the auction.

Before bidding, confirm the state procedure, local sale rules, title risks, redemption issues, financing timeline, and possession expectations.

The better you understand the foreclosure process before you bid, the less likely you are to overpay for a deal that only looked profitable on paper.

Want To Know What Properties Banks Are About To List?

Learn how to find deeply discounted properties. Get instant access to pre-foreclosures, REOs, and short sales updated daily!

You might also like:

Foreclosure Auction Tips That Could Save You Thousands

Foreclosure Auction Tips That Could Save You Thousands

The Complete Foreclosure Due Diligence Checklist for Investors + Free Template

The Complete Foreclosure Due Diligence Checklist for Investors + Free Template

Foreclosure Investing Risks Every Beginner Should Know

Foreclosure Investing Risks Every Beginner Should Know

Title Search for Foreclosure Properties: Investor Essentials

Title Search for Foreclosure Properties: Investor Essentials

Foreclosure Investing: How to Buy, Analyze, and Profit From Foreclosed Homes

Foreclosure Investing: How to Buy, Analyze, and Profit From Foreclosed Homes

How Foreclosure Redemption Periods Affect Investor Profit

How Foreclosure Redemption Periods Affect Investor Profit