How Foreclosure Redemption Periods Affect Investor Profit

A foreclosure redemption period can change the entire profit timeline on a foreclosure deal. Winning the bid does not always mean you can immediately take possession, start repairs, list the property, refinance, or collect rent.

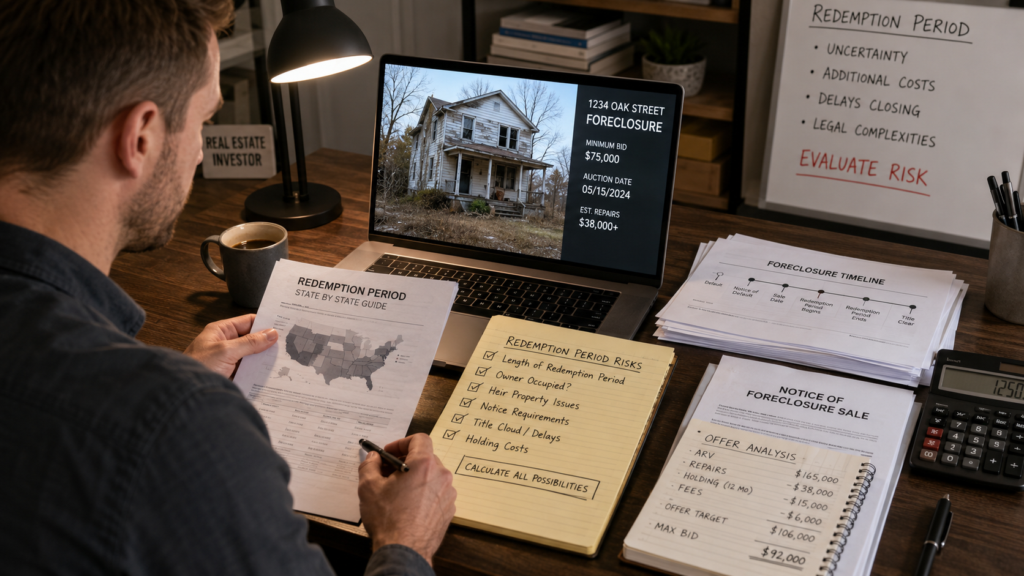

For investors, this is not just a legal detail. It is a holding-cost issue, a financing issue, and a risk-management issue. Before you bid on a foreclosure, you need to know whether redemption rights apply, how long they last, and what they could do to your exit strategy.

Get Foreclosure Investing Insights Twice a Week

Subscribe to the Foreclosure Flips newsletter for practical ideas on finding deals, analyzing opportunities, and understanding foreclosure-related investing strategies. We send concise updates twice a week so you can stay informed without adding more noise to your inbox.

What Is a Foreclosure Redemption Period?

A foreclosure redemption period is a legal window that may allow the former homeowner, borrower, or another qualified party to reclaim the property by paying the required amount.

The exact rules depend on state law, and some states allow redemption before the foreclosure sale while others may allow a limited post-sale right of redemption.

The basic concept is explained in Cornell Law School’s definition of the right of redemption, which notes that state law controls whether and how long these rights continue after foreclosure.

That matters because foreclosure investing is highly local. Two properties with similar purchase prices and repair budgets can produce very different outcomes if one has a short redemption window and the other has a long statutory redemption period.

Why Redemption Rights Can Delay Investor Profit

Possession May Not Be Immediate

The biggest practical issue is control. In some states, the prior owner may remain in possession during the redemption period. FindLaw’s overview of statutory redemption notes that redemption periods can vary widely and that possession rules can affect what happens after the sale.

If you cannot obtain possession quickly, you may not be able to inspect the interior, begin demolition, secure the property, or confirm the true repair scope. That can make your original rehab budget less reliable.

Rehab Work Can Be Put on Hold

Even if you are confident the property will not be redeemed, starting major repairs before the redemption period expires can be risky. If the prior owner redeems the property, you may be forced to unwind the deal based on the state’s rules and the sale terms.

This is especially important for flips. A six-month delay can turn a strong projected return into a mediocre deal once you add loan interest, taxes, insurance, utilities, lawn care, and opportunity cost.

Resale and Financing May Be Harder

A redemption period can also create title uncertainty. Some lenders, title companies, and buyers may be reluctant to move forward until redemption rights expire or are legally resolved.

That can affect your ability to refinance into long-term debt, sell to a retail buyer, or close with another investor. Justia’s explanation of foreclosure redemption rights highlights the difference between redemption before sale and possible redemption after sale, which is the issue most likely to affect investor exit timing.

How to Underwrite a Deal With Redemption Risk

Do not treat the redemption period as a small technicality. Build it directly into your numbers.

Before bidding, confirm:

- The state and county redemption rules.

- Whether the foreclosure is judicial or nonjudicial.

- Whether the redemption period applies after the sale.

- Who can redeem the property.

- Whether you can obtain possession during the redemption period.

- Whether your title company will insure resale or refinance before expiration.

Then add conservative carrying costs to your deal analysis. If your hard money loan costs $2,500 per month and the redemption period could last six months, that is $15,000 in additional holding cost before you even account for taxes, insurance, utilities, maintenance, or delayed resale proceeds.

The Investor Takeaway

A foreclosure redemption period does not automatically make a deal bad. It simply means the deal needs to be priced correctly.

If the potential profit is strong enough to absorb delayed possession, slower rehab work, extended financing costs, and a delayed exit, the property may still be worth pursuing. But if the margin is already thin, redemption rights can erase your profit before the project begins.

The safest approach is to verify the redemption rules before bidding, model the slowest realistic timeline, and avoid using best-case assumptions to justify a foreclosure purchase.

Wondering Where the Savviest Investors Find Their Best Deals?

Access the largest database of foreclosure properties nationwide and discover below-market deals before other investors. Start your search today!

You might also like:

Foreclosure Auction Tips That Could Save You Thousands

Foreclosure Auction Tips That Could Save You Thousands

The Complete Foreclosure Due Diligence Checklist for Investors + Free Template

The Complete Foreclosure Due Diligence Checklist for Investors + Free Template

Foreclosure Investing Risks Every Beginner Should Know

Foreclosure Investing Risks Every Beginner Should Know

Preparing for a Foreclosure Auction: What to Know [Free Download]

Preparing for a Foreclosure Auction: What to Know [Free Download]

Title Search for Foreclosure Properties: Investor Essentials

Title Search for Foreclosure Properties: Investor Essentials

Foreclosure Investing: How to Buy, Analyze, and Profit From Foreclosed Homes

Foreclosure Investing: How to Buy, Analyze, and Profit From Foreclosed Homes