Tax Lien vs Tax Deed Investing for Distressed Deals

Understanding tax lien vs tax deed investing is important before you bid on any tax-delinquent property opportunity. These two strategies sound similar, but they are not the same deal.

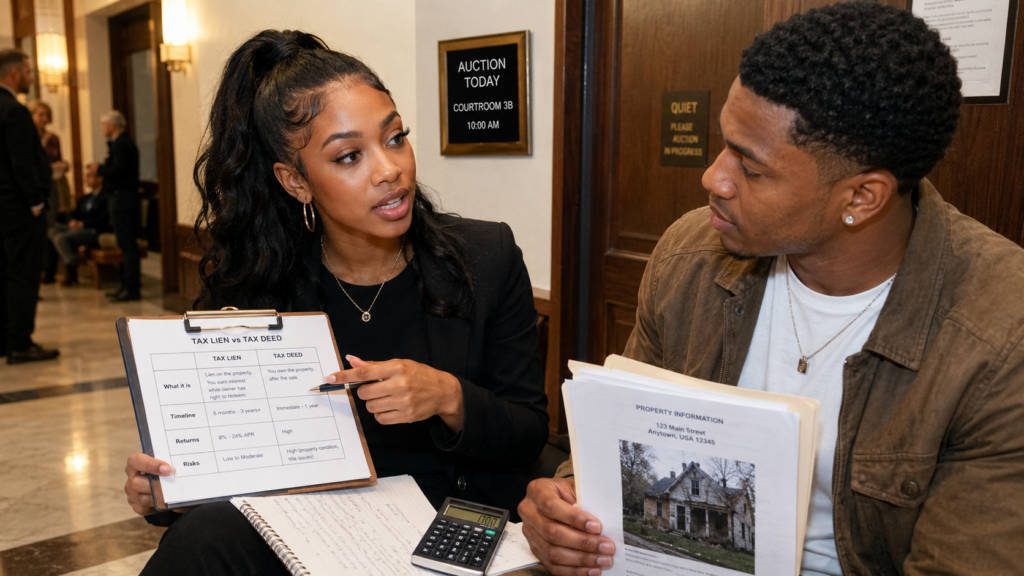

In a tax lien sale, you are usually buying a lien connected to unpaid property taxes. In a tax deed sale, you may be bidding to acquire ownership of the property itself. That difference affects your profit model, timeline, due diligence, title risk, and exit strategy.

If you’re an investor, the first question is not just “Is this property tax delinquent?” The better question is “Am I buying a lien, or am I bidding on the property?”

Get Foreclosure Investing Insights Twice a Week

Subscribe to the Foreclosure Flips newsletter for practical ideas on finding deals, analyzing opportunities, and understanding foreclosure-related investing strategies. We send concise updates twice a week so you can stay informed without adding more noise to your inbox.

What Is Tax Lien Investing?

Tax lien investing usually means you pay delinquent property taxes on behalf of the owner and receive a tax lien certificate or similar instrument. You do not automatically own the property.

Instead, you may have the right to collect repayment, interest, penalties, or eventually pursue additional remedies if the owner does not redeem.

Florida’s delinquent-tax sale guidance makes this distinction clear by explaining that a tax certificate is a lien created by payment of delinquent taxes, not a purchase of the property itself. That same principle is central to the tax certificate investment model.

How You Make Money With a Tax Lien

Your return usually comes from the property owner redeeming the lien. The owner pays the delinquent taxes, plus interest or statutory charges, and you receive the repayment according to local rules.

That can make tax lien investing feel more like a yield strategy than a property acquisition strategy. You may never take possession, inspect the interior, renovate the house, or sell the property.

The risk is that you are still tied to the underlying real estate. If the property has little value, environmental issues, municipal violations, title problems, or no realistic exit path, the lien may be less attractive than the advertised interest rate suggests.

What Is Tax Deed Investing?

Tax deed investing is different. In a tax deed sale, the property itself is sold because property taxes were not paid. If you are the winning bidder, you may receive a tax deed transferring whatever interest the taxing authority or seller can convey.

That does not automatically mean you receive clean, marketable title. Some tax deed sales are buyer-beware transactions.

Pasco County’s tax deed sale guidance states that the clerk’s office makes no warranties about property condition, marketability, title, zoning, outstanding liens, mortgages, encumbrances, or defects that may survive the sale. Those risks are part of the tax deed bidder responsibility.

How You Make Money With a Tax Deed

With tax deed investing, your profit usually comes from acquiring the property below its true value, then creating an exit. That exit might be a resale, rental, wholesale assignment, quiet title and flip, or long-term hold.

Because you may actually acquire the property, your due diligence has to be deeper. You need to research title, occupancy, code violations, access, utilities, repairs, zoning, HOA issues, environmental concerns, and whether title insurance will be available after purchase.

Redemption Periods Change the Strategy

The redemption period is one of the biggest differences between tax lien and tax deed investing.

In many tax lien systems, the owner has time to redeem the property by paying the delinquent taxes and required charges. In some tax deed systems, redemption may continue until a specific point before the deed is issued.

State rules control the details. Iowa’s official tax sale guidance, for example, describes redemption through the county treasurer and notes that additional amounts may accrue under state law. For investors, the point is that tax sale redemption rules can vary materially by jurisdiction.

Why This Matters to You

If you want a cash-flowing lien return, a tax lien certificate may fit your strategy better than a tax deed auction. If you want to acquire distressed property directly, a tax deed sale may be closer to your goal.

But you should not bid on a tax lien expecting immediate ownership. You also should not bid on a tax deed assuming the title is automatically clean.

How State Rules Affect Your Plan

There is no single national tax sale system.

Some states are primarily tax lien states. Some are tax deed states. Some use hybrid processes. Counties may also have their own registration requirements, bidding formats, deposit rules, redemption procedures, and post-sale steps.

Before you bid, confirm:

- Whether you are buying a lien or a deed.

- How long the redemption period lasts.

- What interest or penalty structure applies.

- Whether the property can still be redeemed.

- What liens or claims may survive.

- Whether quiet title may be needed.

- Whether the property is occupied.

- Whether title insurance is realistically available.

This is where disciplined investors separate opportunity from speculation.

Wondering Where the Savviest Investors Find Their Best Deals?

Access the largest database of foreclosure properties nationwide and discover below-market deals before other investors. Start your search today!

You might also like:

Foreclosure Auction Tips That Could Save You Thousands

Foreclosure Auction Tips That Could Save You Thousands

How to Analyze a Multifamily Foreclosure Deal

How to Analyze a Multifamily Foreclosure Deal

How Foreclosure Redemption Periods Affect Investor Profit

How Foreclosure Redemption Periods Affect Investor Profit

How Code Violations Affect Foreclosure Deals

How Code Violations Affect Foreclosure Deals

Auction Houses vs Online Foreclosure Auctions

Auction Houses vs Online Foreclosure Auctions

How Bankruptcy Can Delay an Investment Foreclosure Deal

How Bankruptcy Can Delay an Investment Foreclosure Deal