How to Set a Foreclosure Auction Maximum Bid

Setting a foreclosure auction maximum bid before auction day is one of the most important habits a real estate investor can build. The auction environment can move quickly, and competitive bidding can make a weak deal look better than it really is.

Your maximum bid is the highest price you can pay while still protecting your required profit. It should be based on math, not excitement, ego, or fear of missing out.

Learn the Strategies Behind Smarter Foreclosure Investing

Get practical foreclosure investing content delivered twice a week, including deal analysis tips, strategy breakdowns, useful tools, and new resources from Foreclosure Flips. Sign up to keep learning and spotting better opportunities.

Start With the After Repair Value

The first number is after repair value, or ARV. This is the likely resale value after the property is repaired and market-ready.

Do not use the best comparable sale you can find. Use realistic comps that match the property’s location, size, condition after rehab, bedroom and bathroom count, lot size, and buyer expectations.

Use Conservative Comps

If similar renovated homes are selling between $275,000 and $300,000, your underwriting should not automatically assume $300,000. A disciplined investor may use $285,000 or $290,000 unless the property clearly supports the higher number.

The same discipline behind a real estate investor’s maximum allowable offer framework applies directly to auction bidding. You are not trying to guess what the winning bid will be. You are calculating the highest price that still leaves enough room for repairs, carrying costs, resale expenses, and profit.

Subtract Repairs and a Contingency

The next step is your repair estimate. This should include labor, materials, permits, cleanup, landscaping, utility activation, inspection issues, and code corrections.

Foreclosure properties often come with limited interior access before the auction. That means your repair number should include a contingency. If your visible repairs look like $45,000, you may need to underwrite $55,000 or $60,000 depending on age, occupancy, water damage risk, and neighborhood condition.

A conservative repair budget is especially important when you cannot complete a full inspection before bidding. The less access you have, the more room you need in the numbers.

Account for Liens and Title Risk

A foreclosure auction price is not always your total acquisition cost. You need to understand what liens, taxes, municipal charges, HOA balances, or other encumbrances may survive the sale.

A proper pre-bid title review helps identify ownership history, liens, easements, judgments, restrictive covenants, and other issues that can affect the investment. Even if you are buying with cash, title risk can still reduce profit or delay your exit.

Do Not Bid Without a Title Plan

Before bidding, confirm whether you can obtain a title report, what the auction terms say about liens, and whether title insurance will be available after the sale. If you cannot verify the title risk, your maximum bid should be lower.

This is where inexperienced investors often get into trouble. They focus on the winning bid amount but fail to account for costs attached to the property.

Add Holding, Financing, and Selling Costs

Your bid also needs to absorb the cost of time. Holding costs may include loan interest, property taxes, insurance, utilities, lawn care, security, HOA dues, and maintenance.

Financing can change the numbers significantly. Hard money and bridge loans often include interest, origination fees, service fees, leverage limits, and ARV caps. Understanding hard money loan pricing helps you calculate the real cost of capital before setting your bid ceiling.

Selling costs also matter. Include agent commissions, closing costs, seller credits, transfer taxes, staging, photography, and potential price reductions if the property does not sell quickly.

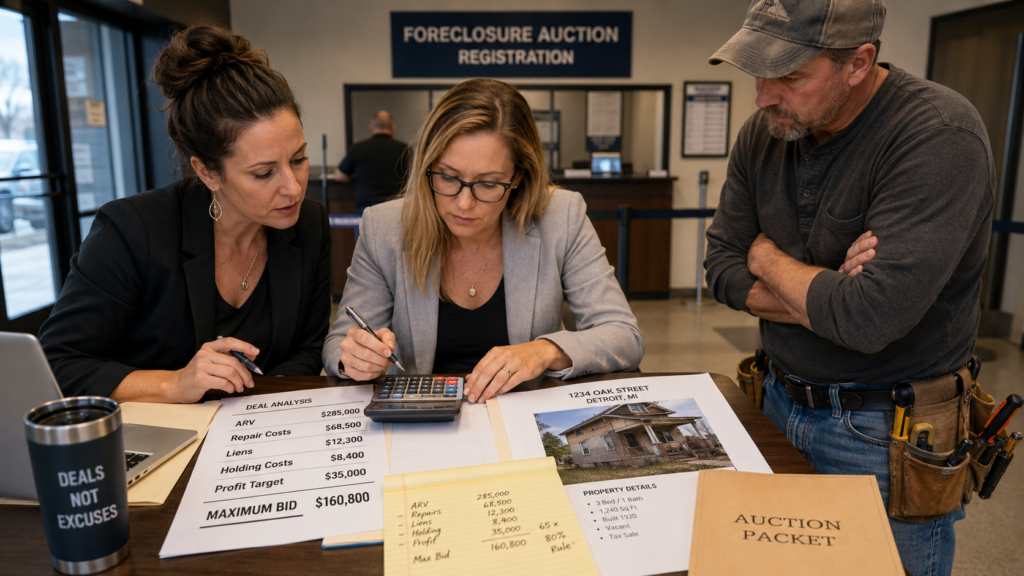

Use a Simple Maximum Bid Formula

A practical formula looks like this:

ARV – repairs – contingency – liens – holding costs – financing costs – selling costs – required profit = foreclosure auction maximum bid

For example:

ARV: $300,000

Repairs and contingency: $65,000

Liens and title risk allowance: $8,000

Holding and financing costs: $22,000

Selling costs: $24,000

Required profit: $45,000

Maximum bid: $136,000

If the bidding goes above $136,000, the deal no longer meets your return requirement.

The Investor Takeaway

Your foreclosure auction maximum bid should be set before the auction begins and followed without exception. The right number protects you from overpaying, underestimating repairs, ignoring title risk, and letting competition control your deal.

A foreclosure auction can create real opportunity, but only when the bid is disciplined. The profit is usually protected before you buy, not after you win.

Looking for Deeply Discounted Properties Others Don’t Know About?

Don’t miss out on the next great investment opportunity! Search millions of foreclosure listings and get daily alerts for new properties in your target market.

You might also like:

Judicial vs Non-Judicial Foreclosure for Investors

Judicial vs Non-Judicial Foreclosure for Investors

What Happens After You Win a Foreclosure Auction

What Happens After You Win a Foreclosure Auction

Title Search for Foreclosure Properties: Investor Essentials

Title Search for Foreclosure Properties: Investor Essentials

Foreclosure Investing: How to Buy, Analyze, and Profit From Foreclosed Homes

Foreclosure Investing: How to Buy, Analyze, and Profit From Foreclosed Homes

Housing Affordability Crisis and Foreclosure Investing

Housing Affordability Crisis and Foreclosure Investing

How Foreclosure Redemption Periods Affect Investor Profit

How Foreclosure Redemption Periods Affect Investor Profit