How Higher Interest Rates Affect Foreclosure Deals

Higher interest rates change the way foreclosure deals work.

They affect what buyers can afford, how much investors pay for capital, how long properties sit on the market, whether a rental property cash flows, and whether a refinance exit still makes sense after repairs are complete. A foreclosure property may appear discounted at first glance, but higher financing costs can quickly reduce the spread between purchase price and actual profit.

That does not mean investors should avoid foreclosure deals. It means they need to analyze them with more discipline.

In a low-rate market, cheap debt and rising prices can hide mistakes. A slightly high purchase price, a missed repair item, or a longer holding period may still be manageable if buyers are plentiful and financing is inexpensive. In a higher-rate market, those same mistakes become more costly. The deal has less room to absorb friction.

For foreclosure investors, the central question is not simply whether the property can be bought below market value. The better question is whether the deal still works after financing costs, repair costs, holding time, buyer affordability, and exit risk are included.

Build Your Investing Knowledge One Email at a Time

Foreclosure investing rewards preparation. Join our 2X week newsletter for straightforward guidance on pre-foreclosures, short sales, BRRRR, flipping, and other strategies investors use to evaluate distressed property opportunities.

Why Interest Rates Matter in Foreclosure Investing

Interest rates matter because most real estate deals depend on debt somewhere in the transaction.

Even when an investor buys a foreclosure property with cash, the end buyer may need a mortgage. If the exit strategy is a flip, buyer affordability affects resale demand. If the exit strategy is BRRRR, the investor’s refinance rate affects cash flow and capital recovery. If the exit strategy is a rental, the loan payment affects whether the property produces income or becomes a monthly drain.

This is why investors should keep an eye on Freddie Mac mortgage rate data. Mortgage rates do not need to spike dramatically to change deal math. Even modest changes can affect monthly payments, buyer qualification, refinance proceeds, and holding costs.

A buyer who could afford a certain home price when rates were unusually low may not qualify for the same price at a higher rate. The purchase price matters, but the monthly payment usually controls the decision. That is especially true for entry-level buyers, who are often the resale target for renovated foreclosure properties.

The same principle applies to investors. A property that looked profitable with cheaper short-term debt may become marginal when hard money, private money, points, insurance, taxes, and delays are added to the model.

Rising Foreclosure Activity Does Not Guarantee Easy Profit

Foreclosure activity has been rising from prior lows. ATTOM’s foreclosure market reports are useful for tracking national and state-level foreclosure filings, starts, auctions, and completed bank repossessions.

More foreclosure activity can create more leads, but lead volume is not the same as deal quality.

A higher-rate market can create distress on both sides of the transaction. Some homeowners may become more motivated to sell, but buyers may also become more cautious. Some lenders may eventually have more distressed inventory to resolve, but investors may face higher capital costs and slower exit timelines.

That makes underwriting more important, not less.

The investor should avoid assuming that a foreclosure discount automatically creates a profitable deal. A property can be discounted and still be a poor investment if the repairs are too high, the resale buyer pool is too thin, the title risk is too great, or the financing costs consume the spread.

The best investors separate market activity from investment opportunity. More filings may create more possibilities, but each property still has to stand on its own numbers.

Higher Rates Reduce Buyer Affordability

The most direct effect of higher interest rates is reduced buyer affordability.

When rates rise, the monthly payment on the same purchase price increases. Many buyers respond by lowering their budget, asking for seller concessions, waiting longer, or leaving the market temporarily. This matters for foreclosure investors because many foreclosure strategies depend on a future buyer.

A flipper may complete a renovation and list the property at a price supported by recent comparable sales. But if buyers in that price band can no longer afford the monthly payment, the property may not move as expected. The investor may have to reduce the asking price, offer closing cost credits, contribute to a rate buydown, or accept a longer holding period.

This is why recent comparable sales are not enough by themselves. In a rate-sensitive market, an investor also needs to understand the behavior of active buyers. A sale from six months ago may not reflect today’s affordability conditions. Pending sales, price reductions, days on market, and seller concessions can tell a more current story than closed comps alone.

The practical question is whether the finished property will be affordable to the likely buyer. If the answer is uncertain, the investor should be careful about paying a price that assumes a fast resale at full after-repair value.

Higher Rates Increase Holding Costs

Foreclosure deals often involve time pressure.

Auction purchases may require quick funding. Bank-owned properties may have strict contract timelines. Pre-foreclosure sellers may need to close before a sale date. Distressed properties may require repairs before they can be resold, rented, or refinanced.

That often pushes investors toward cash, hard money, private money, or other short-term financing. When interest rates are higher, the cost of that capital rises. The investor may pay more in monthly interest, origination points, extension fees, or required reserves.

The danger is not only the higher monthly cost. The greater risk is delay.

A project that takes three months instead of two months may still be profitable. A project that takes seven months instead of four months may look very different. Permit delays, contractor problems, title issues, inspection failures, material shortages, weather, buyer financing delays, and appraisal disputes can all extend the holding period.

In a higher-rate market, investors should calculate the cost of time before they buy. If the deal depends on a perfect renovation schedule and a fast resale, the margin is probably too thin.

BRRRR Deals Become More Sensitive to Debt Terms

Higher rates can be especially challenging for BRRRR investors.

The BRRRR strategy depends on buying below value, renovating, renting the property, refinancing, and holding it as a long-term rental. The refinance step is where the rate environment can create the biggest problem.

A higher refinance rate increases the monthly loan payment. That can reduce cash flow or eliminate it entirely. It can also reduce the loan amount the property supports, especially when the lender is focused on debt-service coverage. If the refinance proceeds are lower than expected, the investor may have to leave more cash in the deal.

That weakens the capital recycling part of the BRRRR model.

A BRRRR deal should be analyzed using today’s financing terms. It should also be tested with less favorable assumptions in case rates rise, the appraisal comes in low, rents soften, taxes increase, or insurance costs jump. The investor should know how much cash is likely to remain in the project after refinance and whether the property still produces acceptable cash flow.

If the deal only works because the investor assumes rates will fall later, the investment thesis is too dependent on macro timing. A future rate decline should be treated as upside, not as the reason the deal works.

Auction Strategy Needs a Wider Margin of Safety

Foreclosure auctions can be attractive because they sometimes offer access to properties below market value. They can also be dangerous because the investor may have limited inspection rights, incomplete title information, uncertain occupancy, and short funding deadlines.

Higher rates make those risks more expensive.

If an investor buys at auction with short-term debt, every month of delay adds carrying cost. If the property needs more work than expected, the additional repair time also adds interest. If the resale market is slower, the investor may have to carry the property longer after renovation. A bid that looked reasonable at the courthouse can become too aggressive once the full timeline is known.

In this environment, auction investors should be careful not to confuse winning with investing well. The winning bidder is often the person willing to accept the lowest margin of safety. That is not always a good position.

A disciplined auction buyer should determine the maximum bid before the auction and stick to it. That bid should reflect not only the estimated value and repair budget, but also title risk, possession risk, financing cost, resale uncertainty, and the possibility of a longer hold.

If another bidder is willing to pay more, the correct decision may be to let the property go.

Short Sales May Become More Relevant

Short sales can become more common when homeowners need to sell but cannot generate enough proceeds to fully pay off the mortgage, closing costs, and other liens. In a short sale, the lender must approve a payoff for less than the full amount owed.

Higher rates can contribute to this situation indirectly. If buyer demand weakens and prices soften in a local market, some owners may have less equity than expected. If the property also needs repairs, the gap between the loan payoff and realistic market value may become wider.

For investors, short sales can create opportunities, but they require patience. The lender will usually need documentation, valuation support, hardship information, and time to review the transaction. Junior liens, tax issues, title problems, or unrealistic lender valuations can delay or kill the deal.

The investor also has to evaluate the exit under current conditions. A lender-approved discount does not guarantee profitability. The property still has to work after repairs, holding time, resale uncertainty, and financing costs.

Short sales are not fast foreclosure deals. They are negotiated transactions where patience, documentation, and accurate valuation matter.

Stay Ahead of the Next Deal

Markets move quickly, and good foreclosure opportunities often require fast analysis. Subscribe to our twice-weekly newsletter for investor-focused tips, tools, and market insights designed to help you make better decisions.

Repair Budgets Need More Discipline

Higher rates make repair mistakes more damaging.

If an investor underestimates repairs, the project may require more cash and more time. More time means more interest, more taxes, more insurance, more utilities, and potentially more extension fees. If the investor over-improves the property, the finished price may exceed what local buyers can afford. If the investor cuts the wrong corners, inspection issues or buyer objections may delay the sale.

The renovation scope should match the exit strategy.

For a flip, the work should support resale value, financing approval, and buyer confidence. That usually means addressing major systems, safety issues, visible condition, and the features buyers expect at that price point. The goal is not to create the most expensive home in the neighborhood. The goal is to deliver a property that sells within the local buyer’s affordability range while preserving investor profit.

For a rental, the renovation should emphasize durability, safety, habitability, and operating efficiency. Materials should be selected for long-term maintenance, not just appearance. A rental property that looks good but requires constant repair can become a weak investment quickly.

For a wholesale exit, the repair estimate still matters. The next buyer will underwrite the project. If the wholesaler’s estimate is unrealistic, the deal will either fail or damage the wholesaler’s credibility.

In a higher-rate market, accurate repair estimating is not optional. It is one of the main defenses against margin erosion.

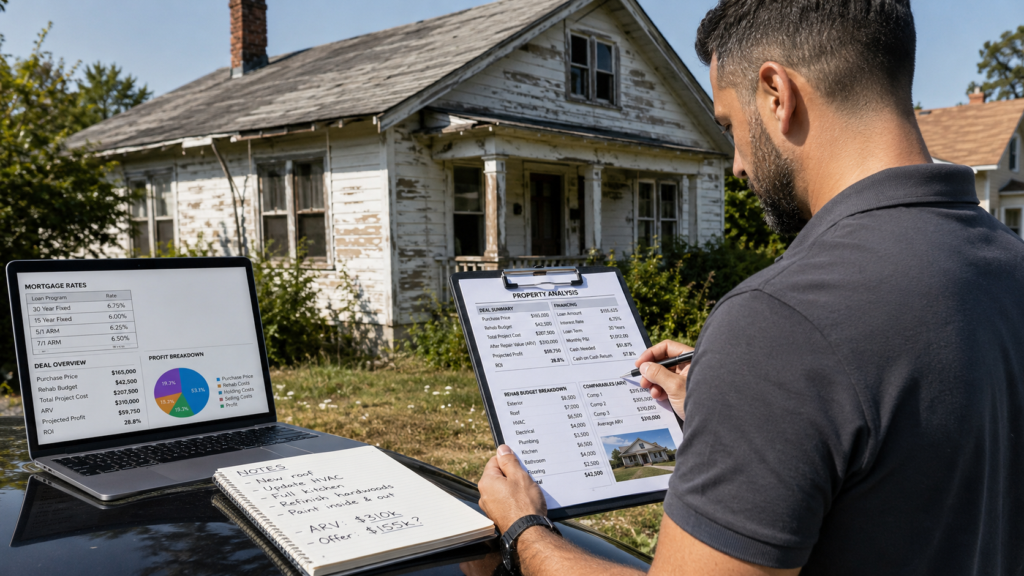

A Better Way to Stress-Test Foreclosure Deals

A foreclosure deal should be stress-tested before the investor makes an offer.

The purpose of a stress test is not to predict the future perfectly. It is to see whether the deal can survive reasonable problems. That matters because higher-rate markets leave less room for optimistic underwriting.

Start with a realistic base case. This should include the expected purchase price, repair budget, financing terms, holding period, resale value, selling costs, and profit. The base case should not be artificially optimistic. It should reflect the deal the investor actually expects.

Then build a more conservative version. Repairs may run higher. The project may take longer. The resale price may be lower. The buyer may ask for concessions. The lender may charge more. Insurance or taxes may be higher than expected.

Finally, identify the break-even point. The investor should know the resale price, rent level, refinance proceeds, or holding period at which the deal stops making money. This is often more useful than the projected profit because it reveals how much room the deal has before it fails.

A tool such as Rehab Valuator can help investors model these scenarios before making an offer. The value is not just in calculating a projected profit. The real value is seeing how quickly that profit changes when rate, repair, rent, resale, and holding assumptions move against the investor.

Higher Rates Should Affect the Maximum Offer Price

Higher rates should usually reduce the investor’s maximum allowable offer.

The reason is straightforward. Higher financing costs, weaker buyer affordability, possible seller concessions, and longer holding periods all reduce the amount an investor can safely pay. Paying the same price in a higher-rate market that would have made sense in a lower-rate market can create unnecessary risk.

For a flip, the investor should start with a conservative after-repair value and work backward. The purchase price has to leave enough room for repairs, financing, holding costs, selling costs, and profit. If the margin only appears after using a best-case resale price, the offer is too high.

For a rental, the investor should start with realistic rent and operating expenses. Then the property should be tested using current financing terms. If the property does not cash flow under today’s debt structure, the investor should not assume refinancing later will fix the deal.

For a BRRRR deal, the investor needs to know how much cash will remain in the project after refinance. A deal that traps too much cash may still be acceptable, but it should be understood before closing.

For a wholesale deal, the property has to be priced so the next buyer can still make money. Higher rates affect that buyer as well.

A lower offer is not necessarily a pessimistic offer. In many cases, it is simply the correct offer for the current capital market.

Higher Rates Can Still Create Opportunity

Higher rates are not only a headwind. They can also create openings for disciplined investors.

Some buyers leave the market when financing becomes more expensive. Some investors pause acquisitions. Some sellers become more negotiable. Some distressed owners need certainty more than maximum price. Some lenders may eventually need to resolve more troubled assets.

That can create opportunity for investors who have cash, financing relationships, local knowledge, and patience.

The strongest opportunities are often not the obvious ones. A move-in-ready foreclosure may still attract heavy competition. A property with repair complexity, title issues, local nuance, or operational problems may be less attractive to casual buyers but workable for an experienced investor.

This is where smaller investors can sometimes compete well. They do not need to outbid every buyer. They need to find situations where their speed, flexibility, local knowledge, or ability to solve a specific problem gives them an advantage.

The key is selectivity. Higher rates should make investors more disciplined, not more aggressive.

Market Indicators Investors Should Watch

Foreclosure investors should watch mortgage rates, foreclosure filings, inventory, buyer demand, and local affordability together. No single metric tells the whole story.

The FRED 30-year mortgage rate series is useful for seeing how rates are moving over time. The National Association of Realtors Housing Affordability Index can help investors understand the relationship between income, home prices, and mortgage qualification.

Those national indicators are helpful, but foreclosure investing is local. County-level foreclosure filings, auction calendars, REO inventory, price reductions, days on market, local employment, insurance costs, tax reassessments, and rental vacancy can all matter more than the national trend.

A market can look healthy at the metro level while certain neighborhoods show stress. The reverse can also be true. A weak metro may still have submarkets where entry-level demand is strong and renovated homes move quickly.

Investors should study the exact buyer or renter who will support the exit. The relevant question is not whether the national market is strong or weak. The relevant question is whether this property, at this price, after this renovation, has a realistic buyer or tenant.

Common Mistakes in a Higher-Rate Market

One of the most common mistakes is using old comparable sales without adjusting for current conditions. A closed sale from several months ago may not reflect today’s buyer affordability, especially if rates, inventory, or concessions have changed.

Another common mistake is focusing too much on the discount and not enough on the exit. A foreclosure bought below estimated market value can still lose money if repairs are underestimated, holding time stretches, or the resale buyer pool is weaker than expected.

Investors also get into trouble when they assume a refinance will solve a thin deal. This is especially risky for BRRRR investors. A rental must be able to support today’s debt, not just the debt the investor hopes to get later.

Overbidding at auction is another recurring problem. Competitive auction environments can push investors into thin margins. The investor may win the property but lose the deal financially.

Finally, many investors underestimate time. Time is expensive when capital is expensive. Every extra month can reduce profit through interest, taxes, insurance, utilities, maintenance, and opportunity cost.

Practical Rules for Foreclosure Investors

A higher-rate market rewards conservative underwriting.

Use current financing terms. Add room for higher costs if the loan will be placed later. Increase the holding-cost estimate rather than assuming a perfect timeline. Use recent comps and current listing behavior, not only older sales. Match the renovation plan to the buyer pool. Verify title, liens, taxes, occupancy, and property condition before committing capital.

Most importantly, require a margin of safety.

A good foreclosure deal should not need perfect execution to be profitable. It should have enough room to survive ordinary problems. Repairs may run over budget. Buyers may negotiate. Lenders may move slowly. Appraisals may disappoint. Contractors may miss deadlines. Markets may soften.

If the deal still works after those risks are considered, it may be worth pursuing. If it only works under ideal assumptions, it is better to pass.

Looking for Deeply Discounted Properties Others Don’t Know About?

Don’t miss out on the next great investment opportunity! Search millions of foreclosure listings and get daily alerts for new properties in your target market.

You might also like:

Buying REO Properties: Essential Guide for Investors

Buying REO Properties: Essential Guide for Investors

REO Property Negotiation Tips for Real Estate Investors

REO Property Negotiation Tips for Real Estate Investors

Selling REO Properties for Maximum Profit: Investor Guide

Selling REO Properties for Maximum Profit: Investor Guide

Foreclosure Investing: How to Buy, Analyze, and Profit From Foreclosed Homes

House Flipping: How to Find, Analyze, Renovate, and Sell a Profitable Flip

Foreclosure Investing: How to Buy, Analyze, and Profit From Foreclosed Homes

House Flipping: How to Find, Analyze, Renovate, and Sell a Profitable Flip

How to Build an Accurate ARV Analysis [Free Worksheet]

How to Build an Accurate ARV Analysis [Free Worksheet]