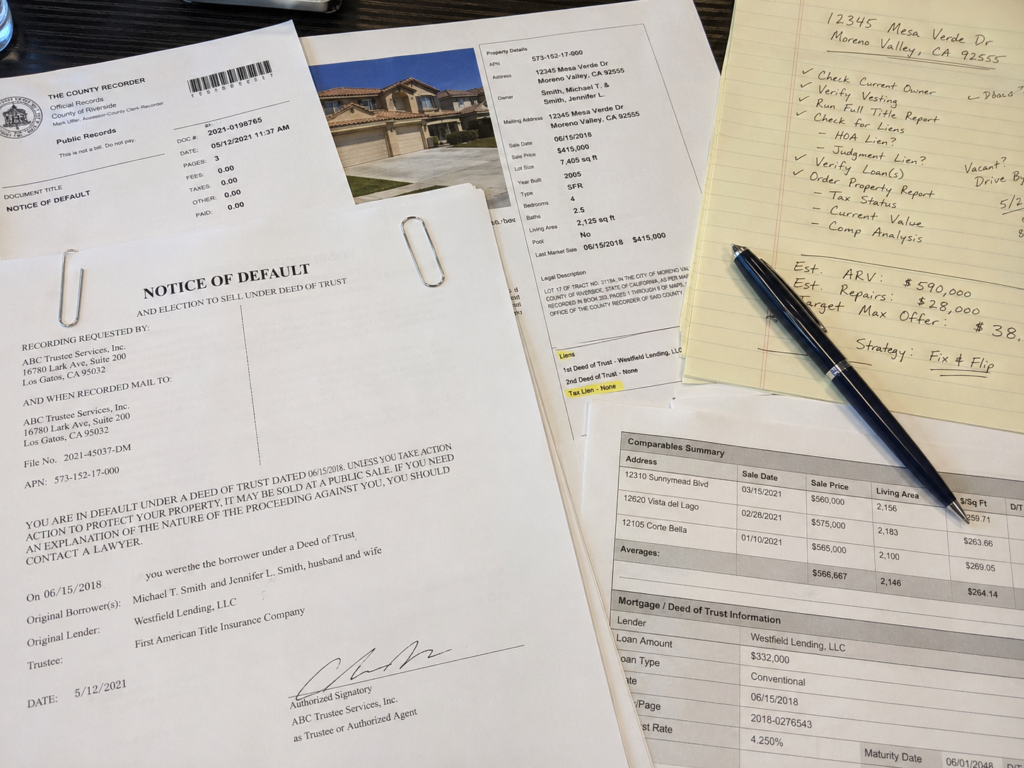

Notice of Default and Lis Pendens: How Investors Find Early Foreclosure Opportunities

Some of the best pre-foreclosure research starts with legal documents. Two of the most important terms investors encounter are notice of default and lis pendens. These documents are not the same, but both can signal that a property may be moving toward foreclosure.

Understanding these records gives investors an advantage. Instead of waiting for a property to appear at auction or become bank-owned, investors can identify potential distress earlier in the process. That can create more time to research the property, evaluate the numbers, and determine whether a voluntary purchase may be possible.

However, these records must be handled carefully. A notice of default or lis pendens does not mean the property is for sale. It does not mean the owner has no options. It simply means a legal or recorded event has occurred that may affect the property.

What Is a Notice of Default?

A notice of default is commonly associated with non-judicial foreclosure states. It is a formal notice that the borrower is in default under the mortgage or deed of trust. Cornell’s Legal Information Institute defines a notice of default as a notice issued when a borrower misses required mortgage payments, often recorded in public records, and signaling that the lender may accelerate the loan or begin foreclosure if the default is not cured.

For investors, a notice of default can be an early distress signal. It may show that the borrower has fallen behind and that the lender has taken a formal step toward foreclosure.

Why It Matters

A notice of default may appear before the auction stage. That can give investors more time to evaluate the property and, if appropriate, contact the owner. The owner may still be able to reinstate the loan, refinance, sell, negotiate with the lender, or pursue other options.

This is why investors should not view a notice of default as a guaranteed buying opportunity. It is a lead, not a deal.

What Is Lis Pendens?

Lis pendens is commonly associated with litigation involving real property. In foreclosure investing, it often appears in judicial foreclosure states where the lender files a lawsuit. Cornell’s Legal Information Institute explains that a lis pendens notice is recorded in the property’s chain of title and alerts third parties to pending litigation affecting title or an interest in the property.

The phrase means “suit pending.” In practical terms, it tells the public that there is litigation connected to the property.

Why It Matters

A lis pendens can affect title. Anyone who acquires an interest in the property after the notice may be subject to the outcome of the litigation. For investors, that means lis pendens records should be reviewed carefully before any offer, assignment, purchase, or closing.

A lis pendens may be related to foreclosure, but it can also involve other disputes. Investors should read the underlying case information whenever possible.

Notice of Default vs Lis Pendens

The key difference is the process.

A notice of default is typically a lender notice related to borrower default and may be used in non-judicial foreclosure states. A lis pendens is a notice of pending litigation and is often associated with judicial foreclosure or other property-related lawsuits.

Both can appear in public records. Both can alert investors to potential distress. But they require different follow-up research.

Practical Difference for Investors

If you find a notice of default, your next step is usually to check the foreclosure timeline, trustee information, loan status, sale date, and property equity.

If you find a lis pendens, your next step is usually to check the court case, complaint, parties, claims, docket activity, and whether the case is actually a mortgage foreclosure.

Where Investors Find These Records

These records may appear in different places depending on the county and state.

Investors may search:

- County recorder records

- County clerk records

- Civil court databases

- Property appraiser records

- Trustee sale notices

- Sheriff sale notices

- Legal publications

- Foreclosure listing platforms

Some counties offer free online search tools. Others charge fees or require in-person access. Listing platforms often aggregate this information, but investors should still verify important details at the source.

How to Evaluate a Notice of Default Lead

Start with the recording date. A recent notice may indicate an active situation. An old notice may have been resolved or replaced by later filings.

Next, check the owner and property address. Confirm that the person named in the notice is still the owner. Then check property value, loan history, liens, and taxes.

Investors should also determine whether a sale date has been scheduled. A notice of default may be early in the process, but a notice of sale may indicate that the timeline is much shorter.

How to Evaluate a Lis Pendens Lead

A lis pendens requires legal context. Do not assume it is a foreclosure just because it involves real estate. Pull the court case if available. Review the plaintiff, defendant, filing date, case type, and docket activity.

If the plaintiff is a mortgage lender or loan servicer, the case may involve foreclosure. If the plaintiff is someone else, the dispute may involve title, ownership, partition, contractor claims, divorce, estate issues, or another real estate matter.

Because lis pendens can affect title, investors should involve a title company or attorney before moving forward.

Why These Records Do Not Guarantee a Deal

Many foreclosure-related filings never result in investor purchases. The borrower may cure the default. The lender may postpone the sale. The parties may settle. The homeowner may refinance. The property may have no equity. The seller may not want to sell.

The Consumer Financial Protection Bureau’s foreclosure overview explains that foreclosure rules vary by state and that borrowers must receive notices as part of the process. Those notices are part of a legal framework, not a sales advertisement.

This is an important mindset shift. Legal distress creates a research opportunity, not an automatic acquisition opportunity.

How Investors Should Use These Records

Investors should use notice of default and lis pendens records as the first layer of a research process.

A practical process looks like this:

- Identify the filing

- Confirm the owner

- Confirm current title status

- Check the property value

- Estimate debt and liens

- Review auction or court timeline

- Determine likely equity

- Evaluate repair risk

- Decide whether outreach is appropriate

The objective is to narrow many filings down to a smaller group of realistic opportunities.

Outreach Considerations

Owners connected to these filings may be under stress. Any outreach should be accurate and respectful. Investors should avoid language that sounds official or threatening. They should not imply that foreclosure is inevitable. They should not provide legal advice unless licensed and qualified.

A professional investor simply asks whether the owner would consider selling and explains that any transaction would be voluntary. If the owner wants help understanding foreclosure options, they can be referred to appropriate legal, lender, or housing counseling resources.

Final Thoughts

Notice of default and lis pendens records are important tools for finding early foreclosure opportunities. They help investors identify properties before auction, understand where distress may be emerging, and build a more targeted acquisition process.

But these records require interpretation. A notice is not a deal. A lawsuit is not a listing. The investor still has to verify the facts, understand the timeline, evaluate equity, and approach the owner professionally.

Used correctly, these filings can become the foundation of a disciplined pre-foreclosure investing strategy. Used carelessly, they can lead to stale leads, legal confusion, and wasted time.

You might also like:

Pre-Foreclosure vs Foreclosure: What Investors Need to Know

Pre-Foreclosure vs Foreclosure: What Investors Need to Know

Pre-Foreclosure Investing: How to Find, Analyze, and Buy Pre-Foreclosures

Pre-Foreclosure Investing: How to Find, Analyze, and Buy Pre-Foreclosures

How to Find Pre-Foreclosure Properties Before Auction

How to Find Pre-Foreclosure Properties Before Auction

Where to Find Pre-Foreclosure Listings Online

Where to Find Pre-Foreclosure Listings Online

How Pre-Foreclosure Leads Work for Real Estate Investors

How Pre-Foreclosure Leads Work for Real Estate Investors

Top Pre-Foreclosure Markets for 2026

Top Pre-Foreclosure Markets for 2026